Price signals and credit penalties in the home insurance market

Jul 10, 2025·

·

0 min read

·

0 min read

Nick Graetz

Abstract

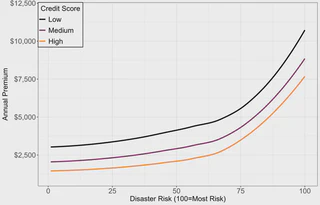

The climate crisis represents an unprecedented challenge for societal risk management, and the home insurance market has come under intense scrutiny as the consequences of climate change have worsened. Insurers argue that pricing according to environmental risk can send price signals to consumers that they can reduce these risks by moving or weatherizing their homes to reduce their prices. But insurers also use individual variables (e.g., credit scores) because they may be predictive of losses (e.g., the likelihood of filing a claim), socially salient, and easy to measure. Still, if there is no causal relationship between credit and the underlying risk of insured events (e.g., hurricanes), then there is no price signal. In other words, individuals will not lower their risk of hurricane damage by increasing their credit scores. If credit penalties are relatively large, they may also crowd out any disaster price signal. In this study, I use standardized industry data on home insurance quotes from 2021-2024 generated using 157 inputs about prospective buyers, including policy details and home characteristics, where all inputs are held constant except credit score and zip code; these quotes represent marginal predictions from the pricing algorithms of home insurers. Disaster risk measured at the zip code level only accounts for 28% of the variance in marginal premiums; most geographic variation is explained by the state of residence. On average, medium credit homeowners pay $792 (39%) more than high credit homeowners for an identical policy; low credit homeowners pay $1,996 (99%) more. The individual credit penalty is equivalent to a 27-point increase in disaster risk rank. My findings challenge the theory that price signaling in the private home insurance market can effectively mitigate the impacts of climate change.

Type

Publication

Working Paper